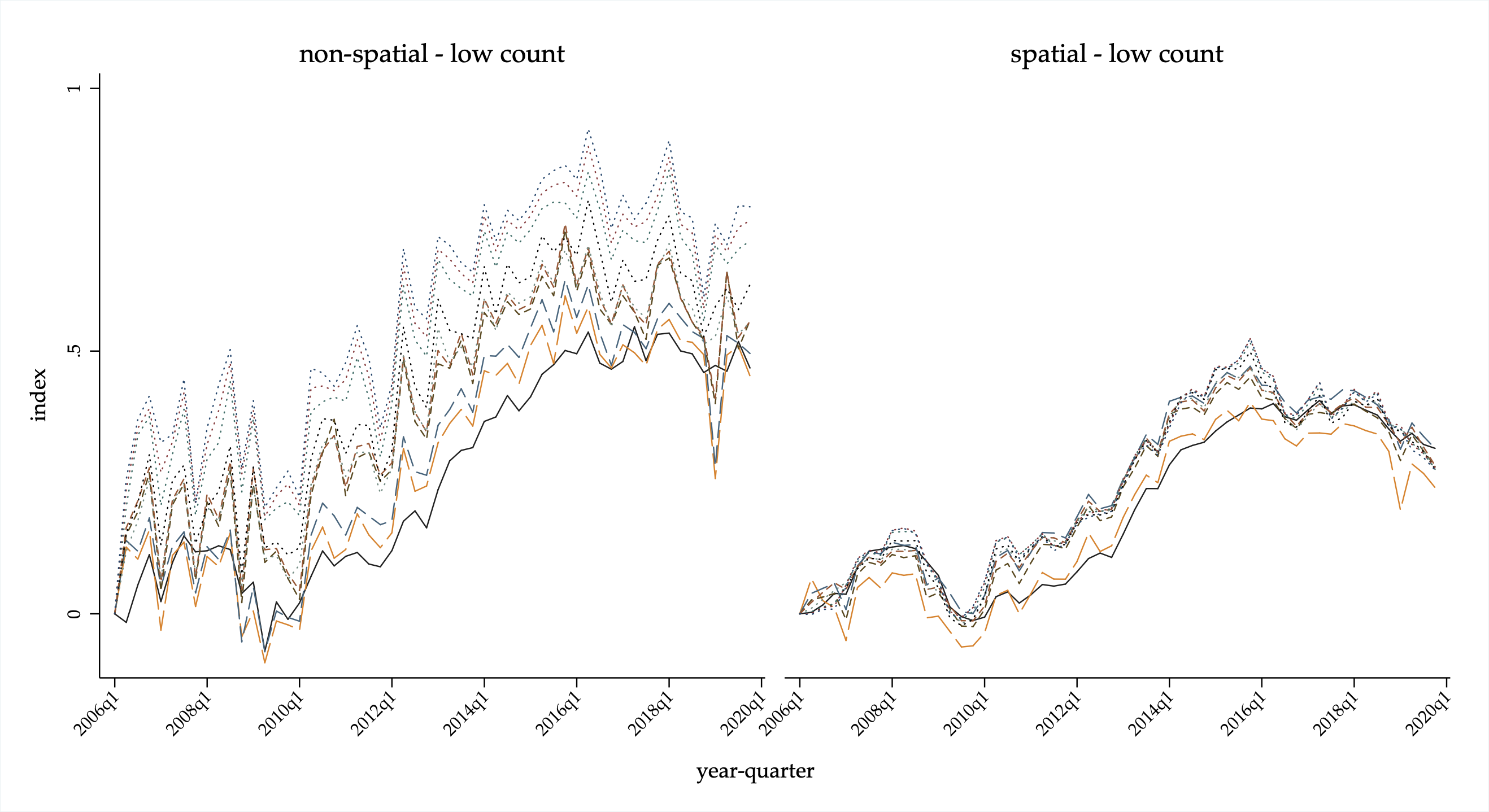

Geographically and temporally granular housing price indexes are difficult to construct. Data sparseness, in particular, is a limiting factor in their construction. In this paper, we introduce a new methodology to construct Census tract level indexes on a quarterly basis that can accommodate sparse data. We augment the repeat sales model with a spatial dynamic factor model. Here, loadings on latent trends are allowed to follow a spatial random walk thus capturing useful information from similar neighboring markets. The resulting indexes display less noise than similarly constructed non-spatial indexes and replicate indexes from the traditional repeat sales model in tracts where sufficient numbers of repeat sales pairs are available. The granularity and frequency of our indexes is highly useful for policymakers, homeowners, banks and investors.

A Spatial Dynamic Factor Repeat Sales Model for Real Estate